PLANULIFE REALTY ANALYSIS

The Canadian housing sector moved from a moderate to high degree of vulnerability during the second quarter, with Toronto, Ottawa and Montreal among the markets at the most risk according to the Canadian Mortgage and Housing Corporation (CMHC).

Home sales reached historic highs in 2021, but there was low evidence of excess inventories. This means that there were not a lot of vacancies among newly built and unsold housing units or rental apartments even though 25% of the housing market is owned by people with multiple properties. Toronto real estate sales may be cooling, but demand is still significantly outpacing supply, and prices are still rising at an increased pace over the sustained period.

The statistics tell us that it’s the suburban areas that are most affected by the overheating. The sales-to-new-listings ratio in the city, where there is plenty of condo supply, is 64%. Meanwhile, more people working remotely pushed the sales-to-new-listings much higher in Durham (86%), Halton (86%) and Peel (81%).

The benchmark home price continued to climb in August, reaching $736,600. That’s a 21% increase from a year earlier, with the cost of homes in Toronto and Vancouver now exceeding $1 million.

EXAMPLE OF A RECENT SALE

28 William Jose Crt.,Newcastle sold by Planulife Realty for $895,450 (up 28% annual) in October 2021

August 2020 value $675,000, up 17%

August 2019 value $550,000

PLANULIFE FINANCING ANALYSIS

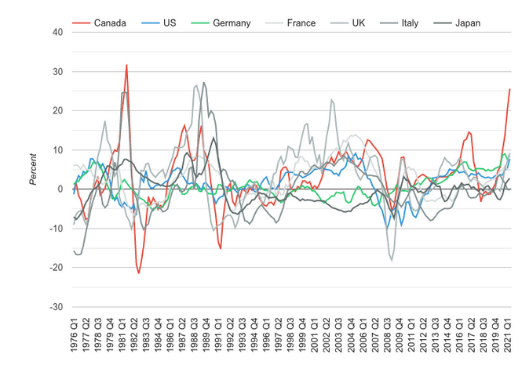

With interest rates expected to go up in 2022 we are predicting the curve will flatten as it did in 2017 when the Bank of Canada implemented the stress test making the qualifying rate 4.79%. This will cause housing prices to stabilize, and supply to meet the demand.

The impact of a 1% hike in interest rate on a $800,000 mortgage on a 25 year amortization is $123,300 over the duration of the mortgage.

| Interest Rate |

Monthly Payment |

Monthly Principal Paid |

Balance Remaining After 5 Year Term |

| 2.50% |

$3,583 |

$1,925 |

$677,103 |

| 3.50% |

$3,994 |

$1,677 |

$690,240 |

| Difference |

$411 |

$248 |

$13,137 |

Even after paying an additional $411 monthly towards your mortgage, since the principal pay down is less, you will still owe over $13,137 more after a 5 year term. The total difference over 5 years is $37,797 ($411*60 months=$24,660 + $13,137).

PLANULIFE INVESTMENTS ANALYSIS

During the pandemic, shocks in global supply chain led to increases in price of labour and material by over 25% in most cases. For example, lumber futures peaked at $1,670 in May of 2021, which was more than double the starting price of $717 at the beginning of 2021. The price increases resulted in significant increases in all pre-construction properties. Additionally, some projects were no longer feasible. In the event of a market decline, construction activity slows and the price of labour and materials stabilizes. This is something we anticipate seeing given that we have already witnessed the peak. These supply chain issues have a direct impact to the lack of supply of new housing in most Canadian markets.

On the other hand, developments that were contracted at pre-covid pricing were built out as planned at normalized rates. What’s shocking is that even at the earlier rates, some investors have not been able to earn healthy returns through pre-construction investing. Here is an example of a recent assignment that came up.

Perla Towers – Mississauga

773 square feet

Available at $615,000 ($796 per square foot)

Original purchase price – $550,000 in 2018

Couple of thoughts here. 1) New condo launches in Mississauga are over $1,200 per square foot. 2) It will cost more than $796 per square foot for a builder to build a similar unit. 3) Despite this, the investor that initially purchased the unit is on pace to only yield $28,000 after expenses [$65,000 gross less closing costs – $30,000, less capital gains tax budget $7,000].

WHAT’S YOUR BEST MOVE?

Downsizers – it may be a good time to cash out of your home. Your Planulife Advisor can review your automated home valuation report with you.

Upsizer or First time home buyer – this is likely the most confusing market in the past decade. Investing now and waiting for the market to settle may be a good option so you get more selection of home options and likely will not have to bid against over 10 people to buy your home. Make sure to login to your Planulife dashboard to review your free Real Estate Financial Plan to review the numbers behind all of your options.

Investors – With multiple properties, right now might be a great time to cash out because higher interest rates will reduce your overall profit. Diversify your portfolio with a pooled investment such as the Planulife Community Redevelopment Fund and earn a 9% secured return tax efficiently through a registered account such as a TFSA or RRSP.

Related stories

Understanding Real Estate Investment Trusts in Canada: The Benefits

Introduction These days investing is getting more popular in Canada and many are now switching to Real Estate Investment Trusts in Canada as a feasible way out. Real Estate Investment Trusts (REITs) are organizations that either own, run or fund rent generating real estate. An individual is able to invest on big income producing properties […]

Winter vs. Spring in the GTA Housing Market

In Real Estate, timing is key. You may have the perfect house to sell, in a desirable location, but if you sell it at the wrong time, you may end up receiving tens or even hundreds of thousands of dollars less than you should. Traditionally, Spring has always been the best time to sell, with […]

Why Invest in Durham?

SUMMARY The Durham Region was ranked #1 for population growth, with continued growth forecast. Durham has the highest growth in Home sale prices in the GTA. Metrolink will be expanding it’s GO Transit network by adding 4 new stations in the region. The region has the most decorated GM plant in all of North America, […]